Member Exclusive

US Actions Trigger Chinese Retaliation Ahead of September Visit

Executive Summary

The US has reaped substantial benefits from increased trade with China in the two decades since China was granted Permanent Normalized Trade Relations (PNTR) status upon accession to the World Trade Organization (WTO). The tariffs imposed by the Trump administration in 2018 using Section 301 of the 1974 Trade Act reversed the decades-long trend of greater US-China trade integration and, according to multiple assessments, including a previous study by Oxford Economics in 2021, hurt US output and jobs.

USCBC commissioned Oxford Economics to build upon our previous study and estimate the economic impact of an escalation of existing tariff measures in the form of revoking China’s PNTR status, a scenario that has been put forward by some in Congress and by three of the leading Republican presidential candidates. In this report, we present the impacts of two such scenarios, one where the US raises tariffs on Chinese imports but faces no retaliation from China (“US tariff-only scenario”) and another which combines the US tariff increase with Chinese policy retaliation, with all other global trade relations remaining at the status quo (“Chinese retaliation scenario”). Below is a high-level overview of estimated impacts relative to our baseline projection which assumes no changes in tariff policy but incorporates the current and expected macroeconomic situation.

Summary of key findings of our model-based analysis:

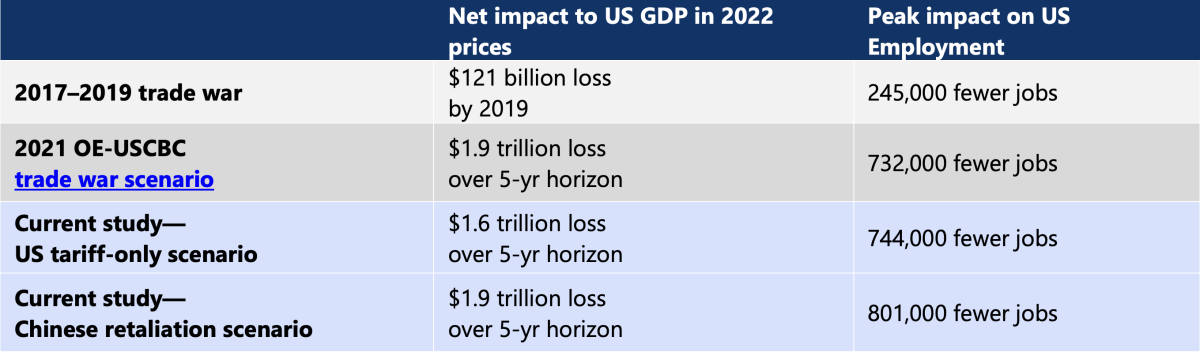

The sixfold increase in US tariffs on imports of Chinese goods since 2018 has reduced both US jobs and output. The deteriorating commercial relationship between the US and China has cut the share of US exports bound for China from 8.6% to 7.5% of total exports between 2017 and 2023. Oxford Economics estimates the losses over the 2018–19 trade war period alone to be about 245,000 jobs (peak impact on a net basis) and $121 billion in output in today’s prices (0.5% of GDP).

The sixfold increase in US tariffs on imports of Chinese goods since 2018 has reduced both US jobs and output. The deteriorating commercial relationship between the US and China has cut the share of US exports bound for China from 8.6% to 7.5% of total exports between 2017 and 2023. Oxford Economics estimates the losses over the 2018–19 trade war period alone to be about 245,000 jobs (peak impact on a net basis) and $121 billion in output in today’s prices (0.5% of GDP).

Further increases to tariffs following a repeal of China’s PNTR status would harm American businesses and consumers and cost up to 744,000 American jobs by 2025 compared to our baseline forecast of no additional tariffs in 2025 beyond existing tariffs today. The US unilaterally raising current tariffs from 19% to 61% would significantly raise prices in the US. We find that US industry, which accounts for the bulk of imports from China, would see input costs rise by 4%, reducing US competitiveness vis-à-vis global peers who would not face any tariff increases. The price of US consumer goods would rise an additional 1.2% in 2024.

An escalation of US tariffs would likely trigger retaliatory measures from China, causing additional US jobs and output losses, pushing the peak impact to 801,000 net job losses by 2025. We assume Chinese tariffs on US exports could rise back to pre-WTO tariffs on top of revoking existing Section 301 retaliatory tariff exclusions, implying a jump from 21% currently to 38%. Our modelling exercise highlights that this would make US businesses less competitive in the Chinese market, resulting in a permanent loss of revenue and pressuring businesses to slash jobs and investment plans.

While some initial pressures would abate as the US economy adjusts, additional tariffs would drive a lasting drop in productivity in both modeled scenarios, leading to permanent US job and output losses. In the likely case of Chinese retaliation, the reduction in US-China trade would cause a cumulative loss of $1.9 trillion in real GDP from 2024–28, with households losing an estimated $11,100 in real income. Despite a recovery from the peak impact in 2025, reduced competition and less efficient allocation of resources would leave a lasting scar on the US economy. We estimate US output would permanently remain 1.4% lower, and there would be 300,000 fewer American jobs on a net basis compared to our baseline forecast (i.e. no additional tariffs beyond existing tariffs today).

Most US industries, but especially consumer-facing ones, would suffer from increased tariffs. Relative to our baseline projection, we forecast a broad-based downturn across US industries in both modeled tariff escalation scenarios, with the magnitude of decline depending on the trade intensity of the sector and the amount of exposure to the Chinese market. While most consumer-facing service industries would encounter headwinds from falling domestic demand, some manufacturing sectors would see output decline by as much as 4.4% if China retaliated.

The economic impact of higher tariffs varies between US states. Nevada, Florida and Arizona would be among the states hit hardest in terms of GDP and jobs, due to the higher importance of consumer sectors in these states. For example, Florida’s GDP would be 1.6% lower by 2025 in the US tariff-only scenario vs. the baseline, with a net loss of 56,000 jobs. Key manufacturing areas of the US would also experience some of the most severe declines, particularly those states with significant automotive, other transport equipment, and machinery industries. This includes Washington and many states in the Midwest and South. Indiana, Kansas, Michigan and Ohio would lose a combined 75,000 jobs on a net basis by 2025 under the US tariff-only scenario. In the Chinese retaliation scenario, the job losses in these four states would increase to 83,000 in 2025.