Member Exclusive

US-China Trade War Tracker

By Yong Teng,Buran Chen

As the economy improves and household incomes rise, Chinese consumers have been demanding higher standards for safety, health, and quality of life. However, there is increasing concern regarding food and drug safety, especially with increasing popularity of purchasing fresh produce online.

Cold chain logistics form the foundation to supply perishable products—fresh fruits and vegetables, meat, dairy, aquaculture products, fresh flowers—and medical products—drugs, reagents, vaccines, biological products—that have strict temperature, humidity, and other environmental requirements.

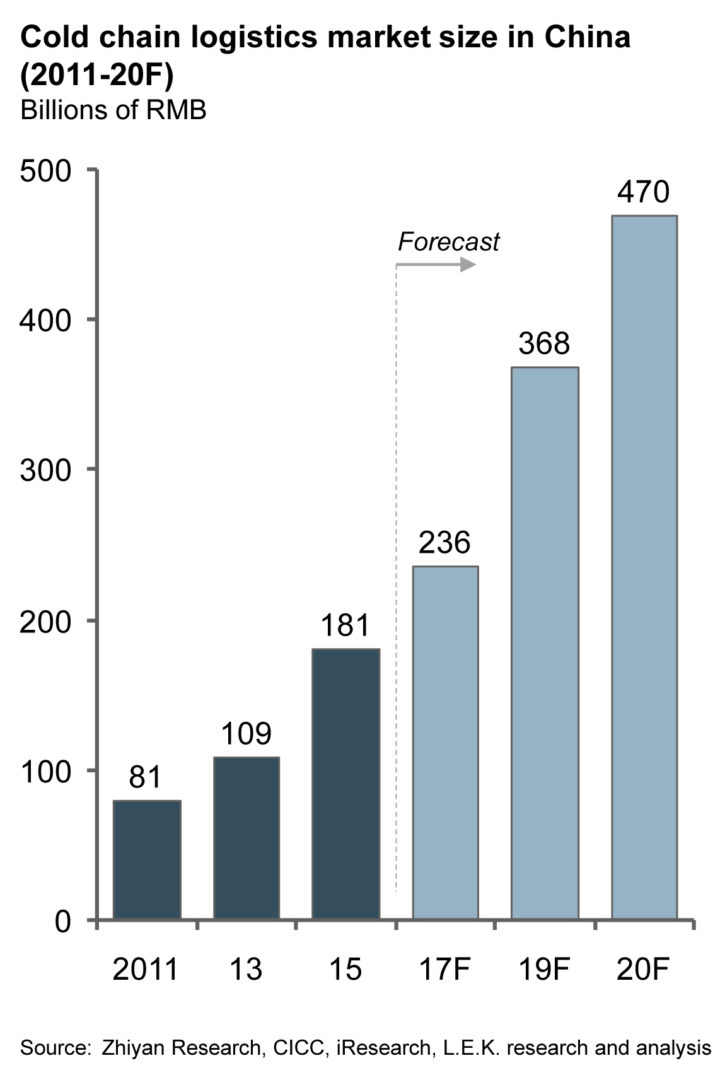

The Chinese cold chain market has grown more than 20 percent over the past five years, increasing from 80 billion RMB in 2011 to 160 billion RMB in 2015. Increasing demand for fresh food and drugs will continue to drive growth in the cold chain industry— L.E.K. Consulting forecasts that the cold chain industry will be valued at 400 billion RMB by 2020, with transportation making up 40 percent of the market, cold storage at 30 percent, and the remainder of the market will be other services.

Figure 1, China’s Cold Chain Logistics Market Size

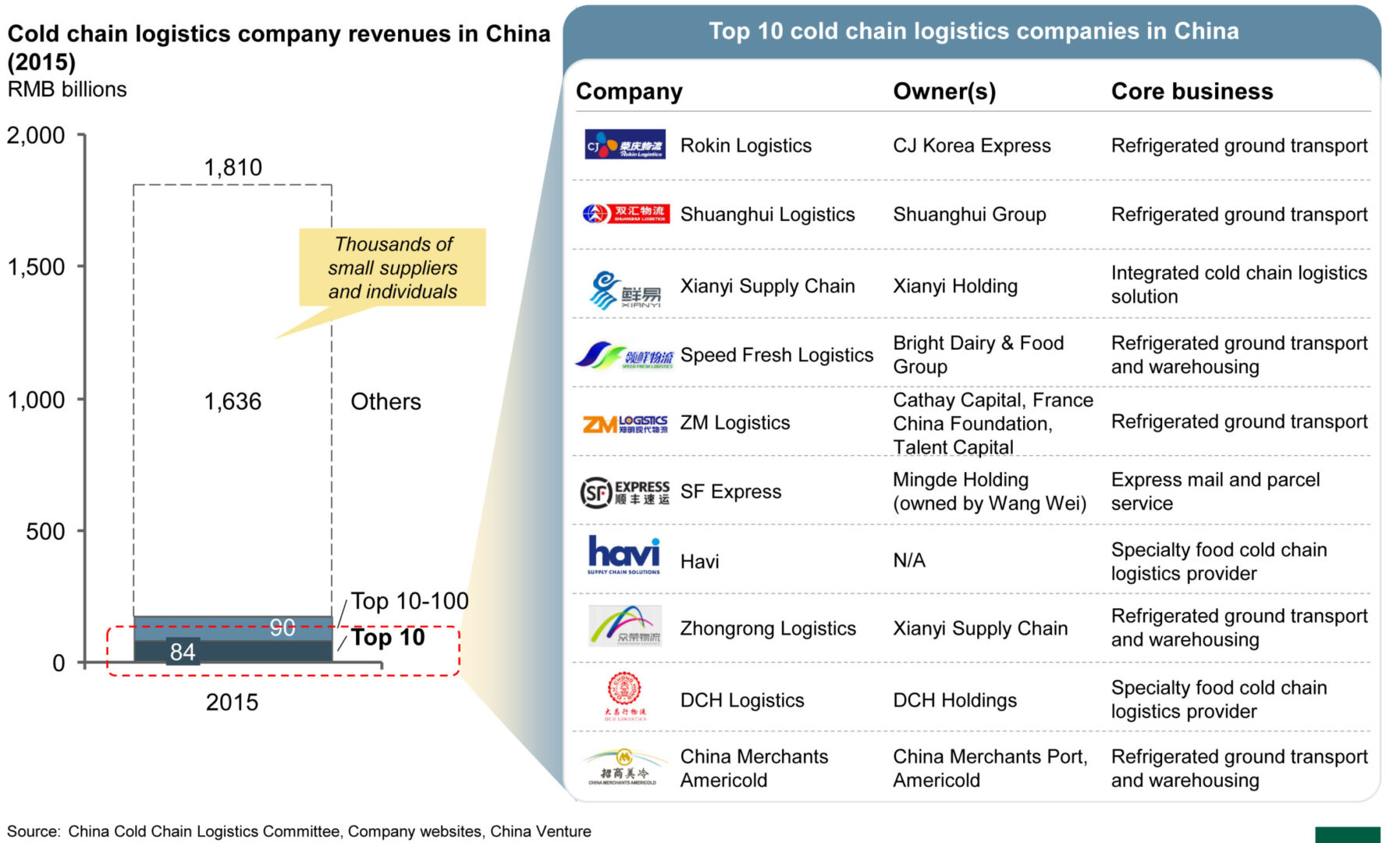

Despite this remarkable growth, the development of China’s cold chain industry is still in its infancy. The market is extremely fragmented; the China Federation of Logistics and Purchasing Cold Chain Logistics Committee estimates that revenue from the top 100 cold chain logistics companies accounts for less than 10 percent of the overall market.

Figure 2, China’s Domestic Cold Chain Market Split by Market Share and Top Ten Players

Although the market is rapidly growing, the unreliability and “breakage” of the cold chain remains a serious problem. As ownership of each stage of the cold chain—warehousing, ground transportation, airfreight, airports, distribution and other services—is fragmented, the lack of an end-to-end process control results in widespread mismanagement of logistics. Additionally, the use of temperature monitoring technology, information systems, and other forms of technical assistance is still very immature. As a result, the rate of cargo damage to fresh product within the cold chain is as much as 20-30 percent—much higher than the average 5-10 percent in developed countries.

In recent years, the Chinese government has worked with industrial associations to jointly introduce a series of standards and policies to regulate and promote the development of the cold chain logistics market. With regards to industry standards, the General Administration of Quality Supervision, Inspection and Quarantine and Standardization Administration of China jointly issued the first Operation Specifications for drug cold chain logistics (GB/T22842-2012) at the end of 2012. In 2014, the National Development and Reform Commission introduced guidelines for cold chain logistics services for aquaculture products (GB/T 31080-2014). At the same time, the International Air Transport Association (IATA) introduced a formal certification, “CEIV Pharma”, for medical logistics projects for China. In February 2016, Shanghai Pudong International Airport was the first and only airport to achieve CEIV Pharma certification. The “No. 1 Executive Order” of the Central Government in 2016 re-emphasized the plan to accelerate the development of cross-region cold chain logistics industry through pilot projects. Hence, L.E.K. Consulting believes that the cold chain industry in China has entered a golden era of development—with many opportunities along each step of the value chain.

Dissecting the Value Chain: Transportation, Storage, Equipment, and 3PL

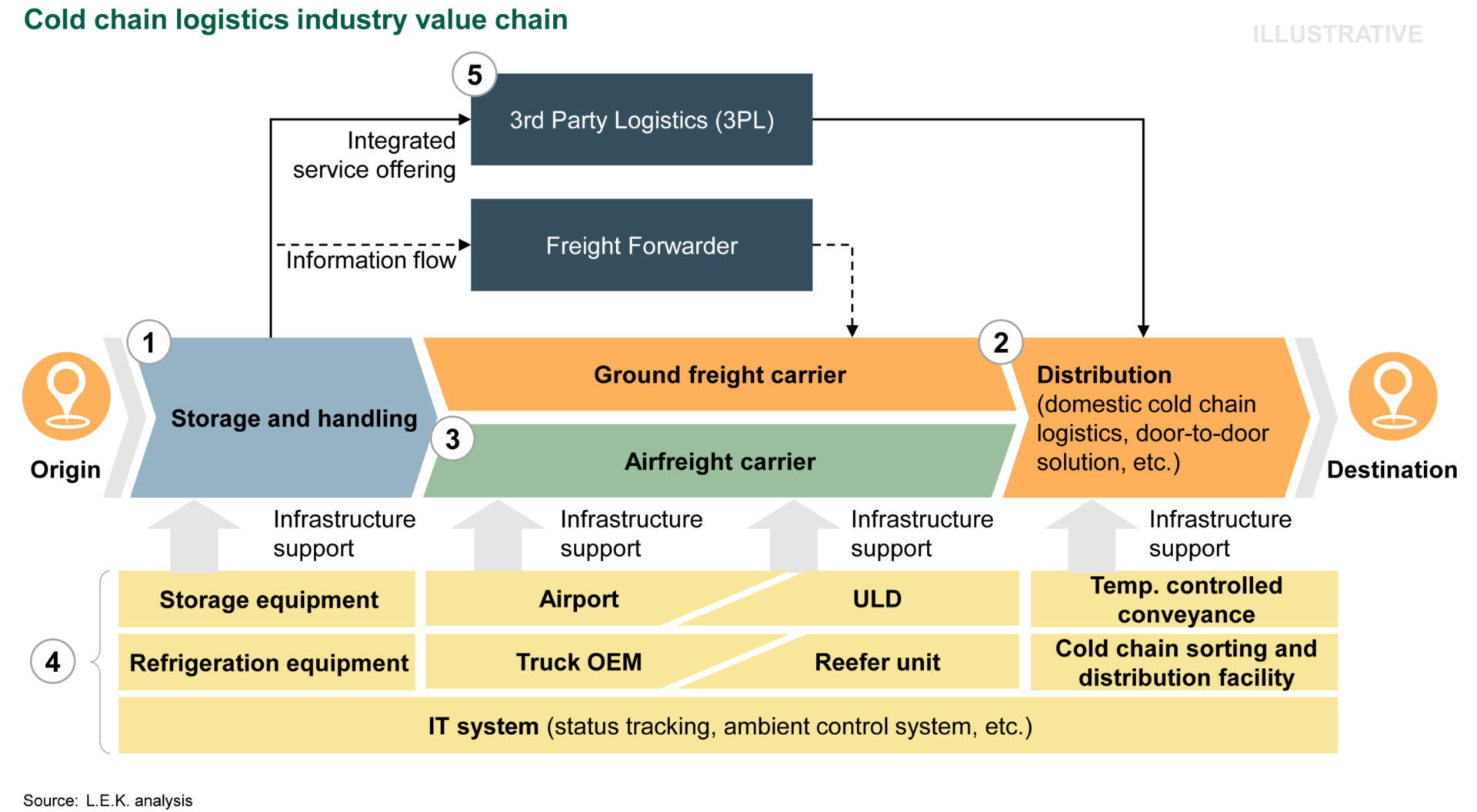

A series of steps are required for temperature-controlled products to move along the cold chain. Cold chain can be broken down into following segments: warehousing, ground transportation, air transport, distribution, infrastructure providers (equipment, systems, basic services etc.), and third-party logistics service providers (3PL).

Figure 3, The Cold Chain Logistics Value Chain

Air and ground transportation in cold chain logistics play different roles due to their respective characteristics. Ground transportation typically involves the use of refrigerated trucks which are highly cost-efficient, flexible and reliable, allow for door-to-door delivery, and have a low cargo damage rate since the temperature-control technology is relatively mature. Conversely, air transportation provides highly efficient and secure transport of goods, but is limited by high costs and limited volumes—and hence reserved typically for high value goods with strict delivery requirements such as drugs, flowers, and expensive aquatic products. However, as the cold chain is easily “broken” in the ground-to-air transportation connection, the use of air transportation potentially carries a higher probability of cargo damage.

Following the development of the cold chain logistics industry, China’s market for temperature-controlled warehousing has also experienced rapid growth. According to the International Association of Cold Storage (IARW), the total national cold storage capacity increased from 13 million square meters in 2008 to 76 million square meters in 2014. Jiangsu Runheng Logistics Development Ltd., Yurun Group, Shandong Yangchun, and Chenzhou Yijie Logistics are the leading domestic players within the cold storage market.

To keep up with the rapid growth of air transportation in the cold chain, a number of temperature-controlled warehouses have been built around airports and the surrounding Airport Economic Zone. Top domestic airports within China with cold storage capacity include Pudong Airport (Shanghai), Baiyun Airport (Guangzhou) and Kunming Airport. Firms such as Xiamen Wanxiang Cold Chain Logistics Centre, Central China Hub of Frozen and Fresh Produce, and Hangzhou Pharmaceutical Logistics Park of Stater Logistics have invested heavily in cold storage infrastructure in the surrounding Airport Economic Zone in recent years.

For ground transportation, there are three types of key market players: traditional trucking companies, fresh produce suppliers or trading companies, and specialty cold chain logistics service providers. Traditional trucking companies such as Rokin Logistics, Zhengming Modern Logistics entered the cold chain market by offering temperature controlled and non-temperature controlled transport services. In the second group, cold chain logistics departments are set up by fresh produce suppliers or trading companies to store and transport large volumes of raw materials or finished products and gradually develop into larger national cold chain logistics companies. Examples of such spinouts include Shuanghui Group’s Shuanghui Logistics, Zhongpin Food’s Xianyi, and Bright Food’s Speed Fresh Logistics. With increasing specialization of cold chain logistics, logistics providers have emerged which specialize in temperature-controlled freight shipping with added features such as long haul transport or last-mile delivery. Domestic players (e.g., Zhongrong Logistics, DCH Logistics), multi-national players (e.g., Havi), and joint-ventures (e.g., China Merchants Americold) are all present in this emerging sector of the market.

Airline companies and large express mail and parcel service companies are the two main cold chain air cargo providers in China. With increasing market demand for high-quality cold chain services, many airlines have set up cargo subsidiaries to provide air cargo services. Airlines expanded their portfolio to provide cold chain courier services by purchasing new cargo aircraft carriers or using the cargo compartment of existing passenger aircrafts to transport goods at low temperatures. Domestic players such as Air China Cargo and China Cargo Airlines use passive temperature controls to provide cold chain transport services, while multi-national companies such as Lufthansa Cargo, Singapore Airlines Cargo, and Emirates SkyCargo offer more customized services based on the nature of the transported goods. Additionally, some large-scale express mail and parcel companies have diversified their offerings to provide cold chain air transport. Three domestic players currently provide cold chain logistics services through their air freight transport fleet—China Post, SF Express, and YT Express. While domestic players mainly provide basic cold chain services, multi-national companies such as FedEx, Ups, and DHL use more sophisticated and integrated IT systems to offer customized cold chain solutions.

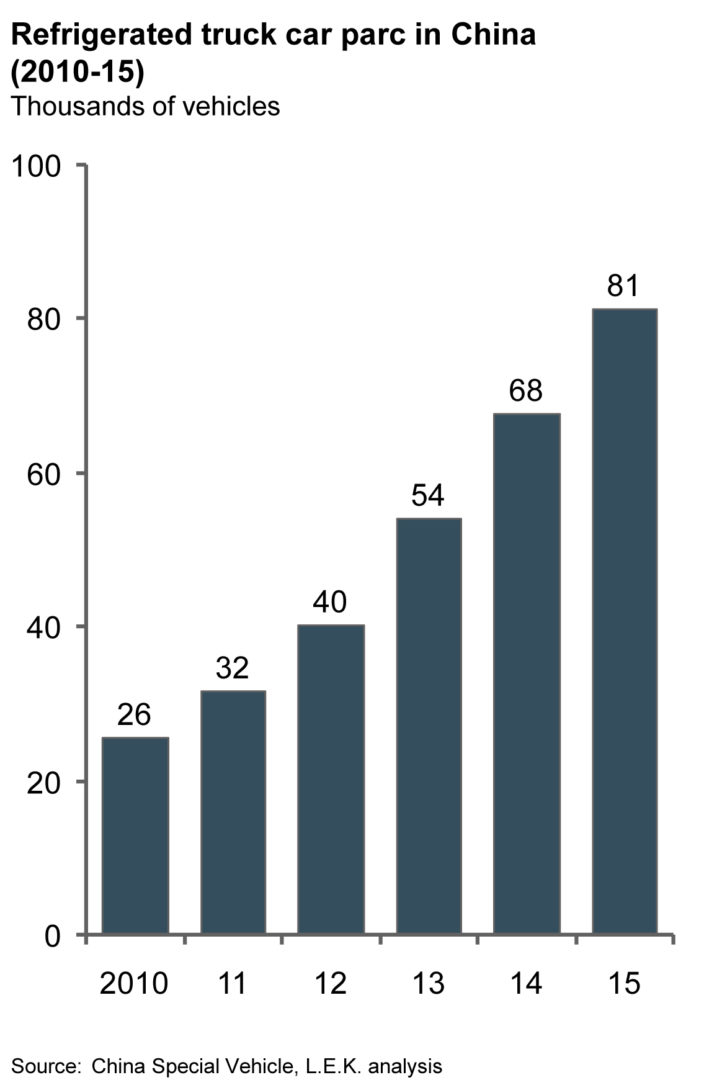

Ground transportation infrastructure has experienced continuous improvement in recent years. Ownership of refrigerated trucks tripled from 26 to 81 thousand between 2010 and 2015. However, the market for refrigerated truck suppliers in China remains fragmented—the top ten suppliers, including Zhenjiang Kangfei Auto and CLW Special Auto, only comprise 26 percent of the market.

Figure 4, Refrigerated Truck Car Parc in China

Domestic cold chain air transportation infrastructure continues to lag behind its international counterparts, especially with regards to temperature controlled containers. Passive ULDs use ice and liquefied gas to control the transport temperature, while Active ULDs make use of refrigerants combined with mechanical or electrical heating and cooling systems to provide more precise temperature control. Envirotainer (Swiss) and Csafe (U.S.) are two leading temperature-controlled ULD multi-national manufacturers; domestic Chinese enterprises have not yet entered this market.

Adoption of active ULDs in China is very limited for three reasons. First, narrow-body airliners make up the majority of China’s airfreight capacity. As active ULDs are larger in size than passive ULDs, the compatibility of active ULDs is limited to cargo aircraft carriers or wide-body aircrafts, which make up less than 15 percent of the market. Second, as the cold chain is easily broken in the ground-to-air connection, improvements in the air cargo temperature control system have little impact on that of the overall cold chain. Finally, as the air cargo cold chain logistics market is relatively new in China, the large upfront investments required to build an active temperature capacity is not yet economically feasible for airfreight carriers in China.

The number of specialty third-party logistics (3PL) cold chain providers offering integrated services have been growing in the recent years. A “one-stop shop” model to offer end-to-end logistics solutions has been favored by the cold chain industry in China. Leading local companies include HNA Cold Chain, Suntone Pharmaceutical Supply Chain, Wuhan Lanesync and Your Logistics. Looking to the future, the cold chain industry will be working towards greater efficiency, optimizing end-to-end logistical progress, providing “one-stop” cold chain solutions, and taking advantage of the rapid growth of 3PL providers.

Identifying the “Hot” Spots For Investing in the Cold Chain

There has been significant M&A activity in ground-based cold chain logistics in China. In 2015, CJ Korea Express, National Pension Service and STIC Investments jointly spent $382 million to acquire China’s cold chain logistics market leader, Rokin Logistics, from Capital Today, Pamoja Capital, and GGV Capital. This acquisition enabled Rokin Logistics to deepen its hold on the domestic market while expanding its logistics capabilities internationally, rapidly improving its market performance. In August 2016, Jinjiang Investment announced their plans to acquire an additional 49 percent stake of Jinjiang Cold Logistics from its prior investor Mitsui & Co. at a price of 147 million RMB—making it the sole owner of Jinjiang Cold Logistics. That same month, Jinjiang Investment announced their purchase of 30 percent of Xintiantian Cold Chain from Mitsui & Co. and Mitsui China. Other notable M&A activity within the ground-based cold chain logistics industry includes a 70 million RMB investment by the CDB Development Fund into HHCold, and a $10 million investment by Ping’an Agri Fund into Express Channel Food Logistics, a regional cold chain provider in Beijing.

Recent transactions also indicate growing investment opportunities along the value chain of airfreight cold chain in China; various airlines have made acquisitions in order to actively expand their cold chain business. In July 2016, Hainan Air Cargo and HNA Aviation Group invested 900 million RMB and 2.8 billion RMB respectively in Yangtze River Express (at 1.6 RMB/share), allowing HNA Aviation Group to own 76 percent of Yangtze River Express after the deal. In the same month, Henan Airport Group and Dalian Port Yidu Cold Chain Logistics jointly initiated the project of Central China Hub of Frozen and Fresh Produce with a total investment of 100 million RMB. Based on the growth of the cold chain industry, future investment opportunities appear most attractive with regards to ULD manufacturing and management, temperature-controlled warehousing, and 3PLs.

As outlined above, the development of China’s cold chain logistics market has entered a golden era. Investors should address the following questions when considering investment opportunities in this sector: Which part of the cold chain logistics value chain has the most potential? What characteristics should investment targets ideally have? What areas will see future growth? What business strategy would allow a company to play a leading role to integrate this industry? How could core competencies be built upon to rapidly improve profitability? Should enterprises position themselves as full service providers or as specialty industry solution providers? Considering these questions will help potential investors accurately grasp the investment opportunities in this golden era.

About the author: L.E.K. Consulting is a global management consulting firm that uses deep industry expertise and rigorous analysis to help business leaders achieve practical results with real impact. The firm advises and supports global companies that are leaders in their industries — including the largest private and public sector organizations, private equity firms and emerging entrepreneurial businesses. For more information, go to www.lek.com. The authors Yong Teng and Buran Chen are both from L.E.K. Consulting’s Shanghai office.